It is crucial to gain a comprehensive understanding of the prevailing trends, challenges, and liabilities construction companies may face.

Below, we will explore the insurance market outlook, focusing on challenges and coverages construction companies may want to consider. By staying informed and adopting proactive risk management practices, construction companies can safeguard their projects, reputation, and financial stability. If you’re planning renewals, start with a full construction insurance review to identify exclusions and contract-driven limit requirements before the market tightens.

Construction Insurance Market Forecast

There are several factors that drove the growth of the construction industry and are expected to continue. One contributing factor is the increased spending on manufacturing-related construction. Another significant driver is the heightened focus on infrastructure investment. Increased spending on roads, bridges, and various clean energy infrastructure projects is anticipated to address critical gaps in the nation’s infrastructure.

Technological advancements, such as 3D printing and robotics, will continue to play a transformative role. These innovations have not only accelerated construction timelines but also aligned with the growing demand for sustainable building practices.

Despite the upward trajectory, the industry still faces a number of challenges. The shortage of skilled workers requires innovative solutions, and the impact of rising interest rates and material costs adds complexity. The Associated Builders and Contractors (ABC) still expects to see an increase in profit margins and staffing levels.

Some additional key trends expected to shape the construction industry in the post-pandemic era include:

- Sustainability: There is a growing demand for sustainable buildings and infrastructure. The construction industry is responding to this demand by developing new technologies and practices that help reduce the environmental impact of construction projects, such as the implementation of green roofs to reduce heat absorption.

- Digitalization: The construction industry is increasingly embracing digital and emerging technologies. These technologies help improve efficiency, productivity, and safety on construction sites.

- Off-site construction: Off-site construction is a broader term that encompasses all forms of construction that take place away from the final building site. This approach can include prefabrication, modular construction, and panelized construction.

Get Commercial Construction Coverage

General Liability & Excess Trends

Liability insurance protects businesses from financial losses if they are sued for negligence or other wrongdoing. There are many different types of liability insurance, each with its own set of coverages. Some of the most common areas of coverage in insurance for construction contractors include:

- General liability insurance: This is the most basic type of construction site insurance for liability. General liability insurance covers claims for bodily injury, property damage, and personal injury.

- Professional liability insurance: This type of insurance covers claims for errors and omissions made by professionals.

- Workers’ compensation insurance: This type of insurance covers employees who are injured or become ill on the job.

- Umbrella liability insurance: This option expands insurance coverage to include claims outside of the insurance’s initial scope.

- Contractors pollution liability insurance: This insurance covers contractors for environmental risks associated with construction for natural and chemical contaminants. For qualifying incidents, contractors can receive coverage for property damage, pollutant removal, bodily injury, and legal defense costs.

Rates have increased for general liability and umbrella liability insurance but have remained consistent for workers’ compensation coverage. The specific areas of coverage needed and their rates depend on occupation, business operations, and personal circumstances. Here are some key factors that affect the cost of liability insurance:

- The type of business

- The size of the business

- The number of employees

- The type of work done

- The business’s claims history

Questions Construction Companies Should Ask of Insurers

With changing insurance rates, obtaining suitable coverage from a reliable insurer is essential. Here are some questions construction companies should consider:

- What types of coverage do you offer? Make sure the insurer offers the project-specific construction insurance coverage needed, such as general liability insurance, professional liability insurance, and workers’ compensation insurance.

- What are your deductibles and premiums? The deductible is paid out of pocket before the insurance company will pay for a claim. The premium is the amount of money paid for the insurance policy each year.

- What are your coverage limits? The coverage limit is the maximum amount of money the insurance company will pay for a claim. The coverage limits should be high enough to protect the business from financial losses.

- What are your claims procedures? If businesses have a claim, they will need to know how to file it and what documentation they will need to provide. Make sure the insurer has a clear and easy-to-follow claims process.

- What is your financial strength? Check the insurer’s financial strength by looking at their ratings from rating agencies, such as AM Best and S&P Global Ratings.

Additional questions to ask about the insurer include:

- What is your experience insuring construction companies?

- Do you have any construction-specific coverages?

By asking these questions and partnering with an agent experienced in the construction industry, businesses can make sure they are getting the best possible insurance coverage. For many contractors, insurance and bonding capacity move together, strong financials and clean loss history can protect both your premiums and your ability to bid larger jobs.

Challenges Facing the Insurance Industry and Construction

A few challenges are impacting property and casualty insurance industry trends. Obstacles in the construction industry are in turn affecting the insurance market.

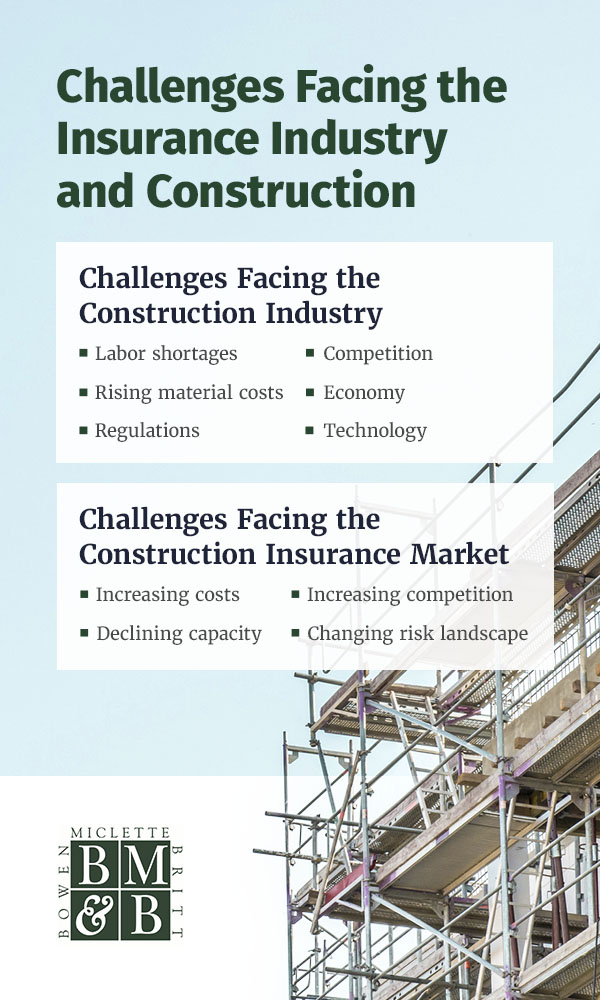

Challenges Facing the Construction Industry

Some risks in the construction industry include:

- Labor shortages: The construction industry is facing a shortage of skilled workers. This is due to a number of factors, including the retirement of baby boomers, the increasing complexity of construction projects, and the lack of training programs.

- Rising material costs: The cost of materials, such as steel and lumber, has been rising in recent years. This is due to a number of factors, including global economic recovery and trade issues.

- Regulations: The construction industry is subject to several regulations, all of which can make it difficult and costly to conduct work. These regulations tend to vary from state to state and from project to project.

- Competition: The construction industry is competitive, with a large number of companies vying for contracts. This can make it difficult to win bids and to turn a profit.

- Economy: Many clients face budget strains and are less open to taking calculated risks in construction investments.

- Technology: The construction industry is slower to adopt innovative technical operations, which often come with additional protocols to protect sensitive data.

The strong demand for housing and infrastructure investment, combined with technological advancements, will help the industry overcome these challenges and continue growing. It is imperative for stakeholders to adopt technological advances and mitigate the financial and potential supply chain risks they may face.

Challenges Facing the Construction Insurance Market

Because of the construction industry’s growth, the insurance sector for this industry is currently facing a number of challenges, including:

- Increasing costs: The cost of construction insurance has been on the rise in recent years. The rising cost of materials and labor, the increasing frequency and severity of natural disasters, and the growing complexity of construction projects have caused rate increases.

- Declining capacity: The availability of construction insurance has been declining in recent years, as insurers have become more cautious about construction insurance underwriting risk. This risk is due to a number of factors, including the rising cost of claims, the increasing frequency of large losses, and the growing complexity of construction projects.

- Increasing competition: Not all insurers are turning away from the construction market. The construction insurance industry is still becoming increasingly competitive, as new insurers enter the market and existing insurers expand their offerings. This competition is putting pressure on prices and making it more difficult for insurers to make a profit.

- Changing risk landscape: The risk landscape in the construction industry is changing as new technologies and materials are introduced and the way that construction projects are managed evolves. This evolution is making it more difficult for insurers to assess and price risk, impacting the average cost of builders risk insurance.

Updates to Construction Insurance Costs

Construction insurance costs have been on the rise. As a result, construction businesses can expect to pay more for insurance than they did in previous years. The exact amount of the increase will vary depending on the type of insurance, the size of the business, and the specific risks involved.

General liability insurance rates may increase this year. These steps can help reduce insurance costs:

- Complying with all applicable safety regulations: This measure will help reduce the risk of accidents and injuries, which can lead to lower insurance premiums.

- Increasing the deductible: By increasing the deductible, businesses can lower their builders risk premium calculation. Keep in mind that this will also increase the amount of money a construction business must pay out in the event of a claim.

- Working with a qualified insurance agency: An agency can help construction companies establish an insurance program that best suits their business and risk appetite.

Business leaders should consider their insurance needs and consult with an agent to determine the policies needed to help reduce their total cost of risk. By taking these steps, construction businesses can better protect themselves from financial loss in the event of an accident or other unforeseen event. Carriers are rewarding contractors who can prove a real loss control program (training, inspections, fleet standards), not just a written safety manual.

Construction Insurance FAQs

Here are some frequently asked questions related to construction insurance:

1. What Is Construction Insurance?

Construction insurance is a type of coverage designed specifically for construction projects. It provides protection against various risks and liabilities that contractors, builders, and other parties involved in construction may face during the course of a project.

2. What Does Construction Insurance Cover?

Construction companies will usually obtain policies that cover a range of risks, including property damage, theft, vandalism, liability claims, and injuries on the construction site. This insurance may also include coverage for materials, equipment, tools, and machinery used in the project.

3. Who Needs Construction Insurance?

Construction insurance is essential for various parties involved in construction projects, including general contractors, subcontractors, builders, developers, architects, and engineers.

4. Is Property Damage Covered Under a Builder’s Risk Policy?

Property damage claims can be covered under a builder’s risk policy if the damage occurred to the insured’s property during the course of construction. However, there are instances where your business might not be protected under this type of policy. You would need to consider a liability policy to protect your business if an employee happened to cause damage to a third party’s property.

5. What Is Liability Insurance in Construction?

Liability insurance protects against claims and lawsuits arising from bodily injury or property damage caused by construction activities. This insurance may cover legal defense costs and settlements or judgments awarded to the injured party. Common liability risks in construction include slip and fall accidents, faulty workmanship, and damage to neighboring properties.

6. Are Subcontractors Covered Under Construction Insurance?

Subcontractors are typically required to have their own insurance coverage, including general liability insurance and workers’ compensation insurance. Additionally, the main contractor may request proof of insurance from subcontractors as part of the contract requirements.

7. How Much Does Construction Company Insurance Cost?

The cost of construction insurance varies depending on several factors, such as the scope and size of the project, the type of coverage needed, the location, the contractor’s experience, and the insurance provider. We recommend partnering with a broker to evaluate the top construction insurance companies. Consider the coverage limits, deductibles, and policy terms when comparing costs.

Get the Preferred Insurance for Construction Companies

As construction companies navigate the dynamic landscape of the industry, effectively managing liability risks is of paramount importance. As one of the Top 100 Brokers, Bowen, Miclette & Britt Insurance Agency, LLC can help find the right insurance for construction companies. Reduce incident frequency and total cost of risk with loss control services—safety training, site audits, and program design.

Contact us to get a quote and discuss the specific coverages available. For jobs with pollution exposure, add environmental liability to address cleanup, third‑party injury, and defense costs.